Welcome back to our Interest Rates Watch series, developed to provide timely updates and practical advice on developments related to interest rates and benchmarks on a regular basis. As always, we are here to help.

The Canadian Alternative Reference Rate Working Group (CARR) has announced that the Canadian Overnight Repo Rate Average (CORRA) term rate (Term CORRA) will be launched on September 5, 2023. Term CORRA has been designed to serve as an alternative benchmark to the Canadian Dollar Offered Rate (CDOR), which will no longer be published following a final publication on June 28, 2024. Term CORRA will be offered initially in one- and three-month tenors.

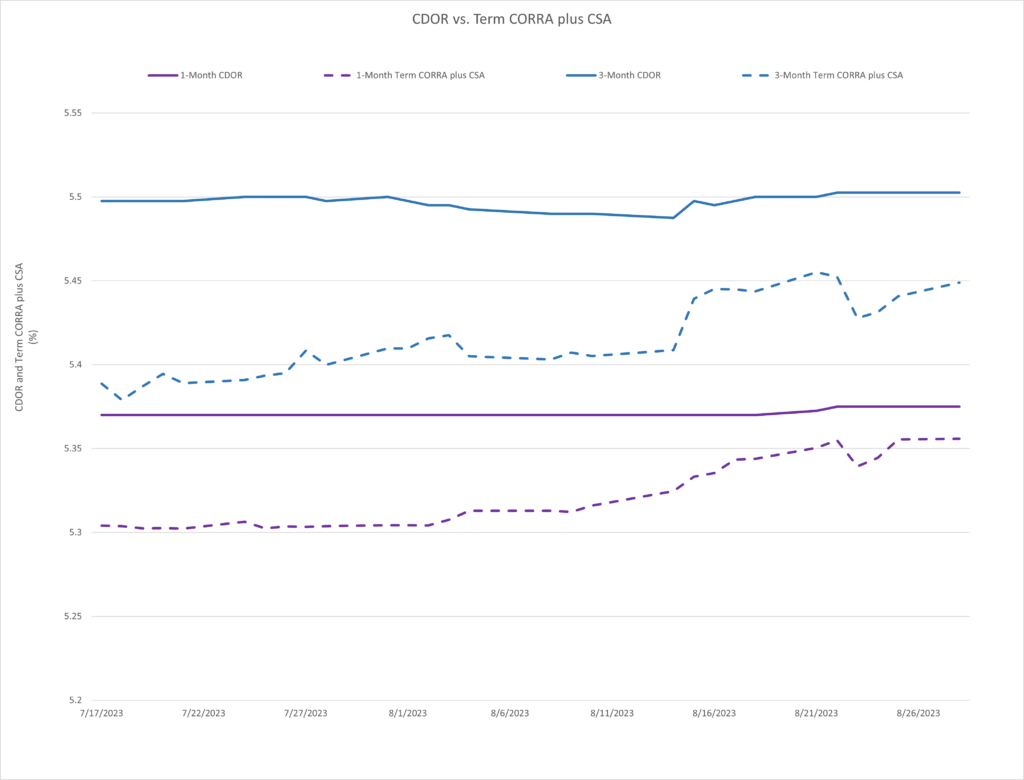

In advance of Term CORRA’s official launch date, CanDeal Benchmark Administration Services Inc. has published a beta version of Term CORRA. While the beta version of Term CORRA is undergoing final testing before its official release on September 5, 2023, the beta version of Term CORRA provides some insight on possible early trends in the economic difference between CDOR and Term CORRA.

In connection with the June 2024 CDOR cessation, many credit facilities have incorporated CARR’s recommended fallback language, which provides that on CDOR’s cessation CDOR-based loans will transition to a CORRA-based rate. To account for the economic difference between CORRA and CDOR, CARR’s recommended fallback language includes a credit spread adjustment (CSA) of 0.29547% (29.547 bps) for a one-month tenor and 0.32138% (32.138 bps) for a three-month tenor (the Fallback CSAs). The Fallback CSAs are expected to result in a CORRA-based rate close to CDOR in the long term. Based on recent beta Term CORRA values, while Term CORRA plus the Fallback CSAs (which are used in the CARR-recommended fallback language) does yield a replacement rate that is close to CDOR, that replacement rate is currently lower than CDOR.

As an alternative to using the Fallback CSAs, market participants may consider one of the following:

- Use a different spread adjustment entirely, similar to the approach seen in the transition from the USD London Interbank Offered Rate (LIBOR) to the forward-looking term rate based on the Secured Overnight Financing Rate.

- Incorporate a transition period (e.g., one year) to gradually move to the Fallback CSAs.

- Replace CDOR with Term CORRA, with no adjustment.

Market participants should consider whether an alternative approach to spread adjustments makes sense from a commercial perspective and should ensure that documentation is amended to provide for the desired fallback rate prior to the cessation of CDOR.

We will be issuing further articles relating to interest rates. Find other articles in our Interest Rates Watch Series here.

#interestrateswatch